Wednesday, 20 May 2026 07:00 AM

Product Announcements

RUGGELL, LIECHTENSTEIN AND VIENNA, AUSTRIA / ACCESS Newswire / May 20, 2026 / On May 20, 2026, this year's In Gold We Trust report was presented at an international press conference broadcast live on the Internet, celebrating its 20th anniversary. The authors of the report are Ronald-Peter Stöferle and Mark J. Valek, fund managers at Liechtenstein-based asset manager Incrementum AG.

The 460-page In Gold We Trust report is renowned worldwide and was honored by the Wall Street Journal as the "gold standard of all gold studies." Last year's edition has been downloaded and shared more than 2 million times. This makes the In Gold We Trust report the most widely read gold study in the world. In addition to the German and English versions, the compact version of the report has been published in Chinese, Spanish, and Japanese for several years.

The In Gold We Trust report 2026 covers the following topics, among others:

20 years of In Gold We Trust: two decades of gold market analysis against the backdrop of historical upheavals

Theme: Back to the Monetary Future, or: the creeping remonetization of gold

The end of the Pax Americana and the tectonic shifts in the global monetary order

The six vectors of gold remonetization - from reserve policy to tokenization

Why the next major surge in gold demand could come from the global bond market

A deep dive by Izabella Kaminska into Tether, a major new player in the gold market, including an interview with Juan Sartori

Performance gold: silver, mining stocks, and commodities remain in the wake of the gold rally

Gold and Bitcoin: stability meets convexity

Update on the proprietary Incrementum gold price model

The conservative 10-year target of USD 4,800 was already reached in 2026 - now the focus shifts to the inflationary scenario of USD 8,900.

Discussion with analysts Luke Gromen and Craig Tindale on the future of the global monetary order and the distortions in commodity markets

Interview with Dr. Judy Shelton on the future of the US dollar and her proposal for gold-backed "Treasury trust bonds"

Key takeaways from the In Gold We Trust report 2026

"Back to the Monetary Future" - the creeping remonetization of gold

The central theme of this anniversary edition encapsulates the essence of twenty years of gold market analysis: The future of money lies in its past. The Pax Americana and the 1971 fiat regime are increasingly showing signs of fatigue. At the same time, gold is gradually regaining monetary significance - not through political decrees but through its function as a neutral store of value and a trust-independent asset.

Gold continues to gain monetary significance

The price of gold has followed an impressive trajectory since the first In Gold We Trust report in 2007. At that time, gold was trading at around USD 670; since then, the price has increased more than 8-fold. Since the "Golden Decade" proclaimed in the In Gold We Trust report 2020, the gain has been around 165%. This development confirms our central thesis: In periods of monetary, fiscal, and geopolitical instability, gold gains importance as a noninflationary asset with no counterparty risk.

Government bonds are losing their sacrosanct status

Excessive debt, structurally higher inflation rates, fiscal dominance, and increasing politicization are increasingly calling into question the status of government bonds, in particular, as a supposedly risk-free asset class. The stock-bond correlation is positive again, real bond yields are under pressure, and the danger of a lost decade for traditional 60/40 portfolios is palpable. This is leading international investors to rethink diversification, value preservation, and strategic gold allocations.

Inflation and debasement risks remain elevated

The waves of inflation in recent years have shown that price stability can no longer be taken for granted. Fiscal dominance, high debt levels, and political incentives for currency devaluation are key arguments for why the risk of further inflationary spikes remains. In the age of the debasement trade, noninflatable assets are evolving from "satellite investments" to "core investments."

Gold, commodities, and Bitcoin: assets with further upside potential

Silver, mining stocks, and commodities remain complementary investments in the gold bull market. Silver has hit numerous new all-time highs. Despite improved fundamentals, the mining sector still accounts for only about 1% of global stock market capitalization. Strategic commodities are likely to increasingly benefit from geopolitical shifts and the expansion of energy, defense, and infrastructure capacities. Bitcoin also remains an attractive portfolio component as a digital, noninflationary asset.

The new 60/40 portfolio is gaining importance

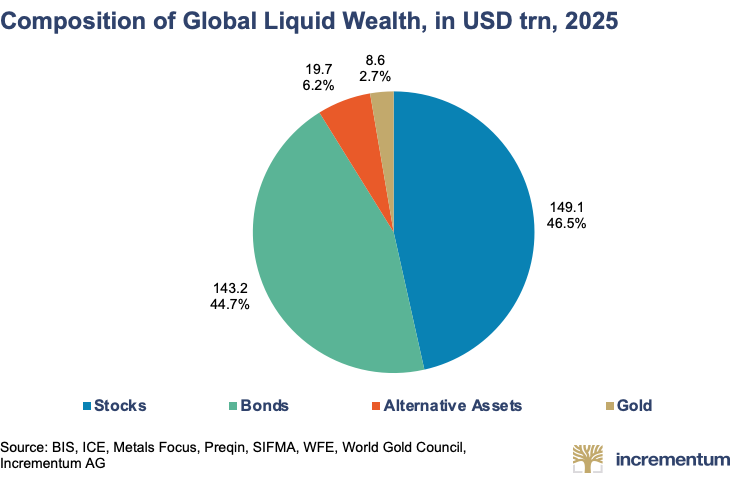

The "new 60/40 portfolio" presented two years ago remains relevant today. Despite its long-term performance, gold remains structurally underrepresented: global financial assets of approximately $312 trillion are offset by only about $8.6 trillion in privately held gold. The fact that Morgan Stanley is now also promoting a "60/20/20" portfolio with a significantly higher weighting in gold underscores the potential for further gold reallocations.

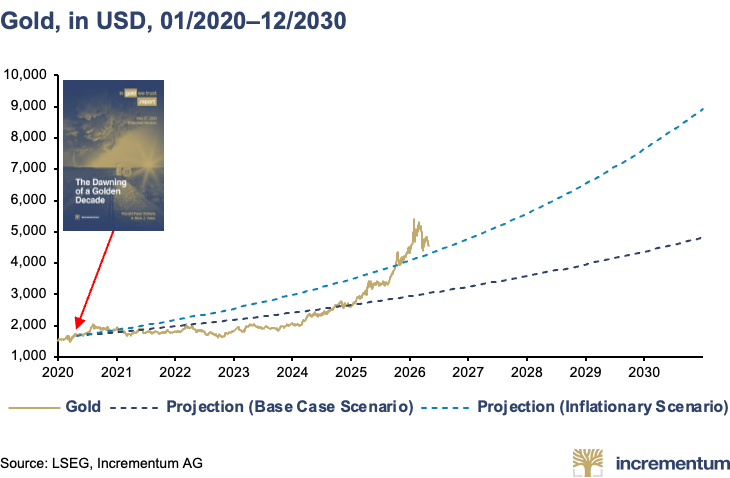

Conservative target of USD 4,800 already reached - USD 8,900 as the next target

The conservative decade-long target of USD 4,800 by 2030, as outlined in the 2020 In Gold We Trust report, has already been reached. In line with the geopolitical macro environment, attention is now increasingly turning to the inflationary scenario of USD 8,900 by the end of the decade. Should current remonetization trends continue to intensify, the authors consider significantly higher gold prices to be conceivable. In the short term, however, there remains a risk of setbacks, especially given rising yields and increased market volatility.

Back to the Monetary Future: 20 Issues of In Gold We Trust

When Ronald-Peter Stöferle published the first issue of the In Gold We Trust report as an analyst at Erste Group in 2007, gold was trading at around USD 670 per ounce. The world was at the height of the Great Moderation: Inflation was considered defeated, government bonds risk-free, and central banks the all-powerful guarantors of economic stability. Terms like quantitative easing, negative interest rates, or financial repression were unknown at the time. Nearly two decades, several crisis cycles, and thousands of pages of analysis later, a completely different picture has emerged. The price of gold has increased more than 8-fold, hitting new all-time highs of USD 5,595 and €4,453. At the same time, global debt has risen to record levels, while confidence in the stability of the existing monetary order is increasingly showing cracks.

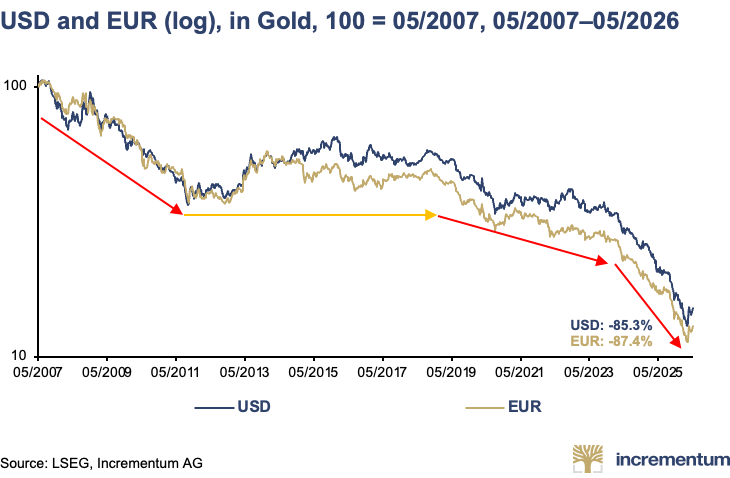

"The past twenty years have shown that monetary and fiscal policy certainties are by no means static," explains Ronald-Peter Stöferle. "Many developments that still appeared to be temporary exceptions after the 2008 financial crisis have since become structural components of the system. At the same time, the US dollar and the euro have lost around 85% of their value against gold since the first edition of the report."

According to the authors, the theme of this year's anniversary edition - "Back to the Monetary Future" - captures the essence of twenty years of gold market analysis: The future of money lies in its past. The Pax Americana and the fiat regime of 1971 are showing signs of strain, while gold is gradually regaining its monetary significance.

"We are not witnessing a return to the classical gold standard," says Mark Valek, who is contributing to the report as a co-author for the 14th time. "But we are certainly observing, in a sense, a remonetization of gold - driven by the actions of many central banks, regulatory developments, and a growing need for neutral reserve assets."

A Changing World Order

The authors of the study see the global monetary and currency order in flux. Geopolitical tensions, trade conflicts, high debt, and the increasing fragmentation of the global economy have ushered in an "interregnum" - a transitional phase in which the old order is losing stability while the new one has not yet been defined. Characteristic features of this include increased volatility, geopolitical uncertainty, and a growing politicization of money, trade, and capital flows.

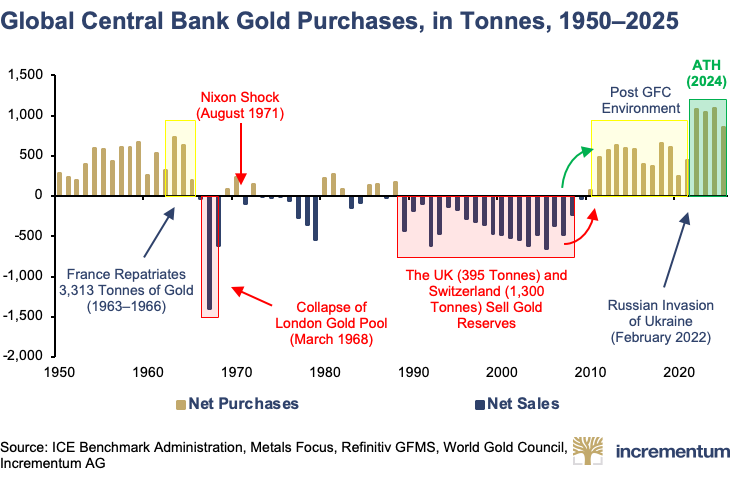

"We are moving from a unipolar to a multipolar world order," explains Ronald-Peter Stöferle. "This is also changing the rules of the game for the international monetary system." This shift is particularly evident in central banks' gold purchases. Since 2010, they have accumulated approximately 9,700 t of gold, more than 4,000 t of which were purchased between 2022 and 2025 alone. In 2025, central banks purchased 863 t of gold worth approximately USD 95.2bn. In Q1/2026, a net additional 244 t were added.

According to the two fund managers, this is not only a reflection of geopolitical uncertainty but also an indication of dwindling confidence in unbacked fiat currencies and traditional reserve assets. "Gold has no counterparty, no political promise, and no issuer risk," says Mark Valek. "It is precisely these characteristics that are regaining strategic importance in an increasingly fragmented world order." Stöferle and Valek emphasize, however, that they do not expect an abrupt collapse of the existing system. Rather, they describe a gradual transition process in which gold is regaining monetary relevance step by step - functionally and market-driven, not ideologically or politically mandated.

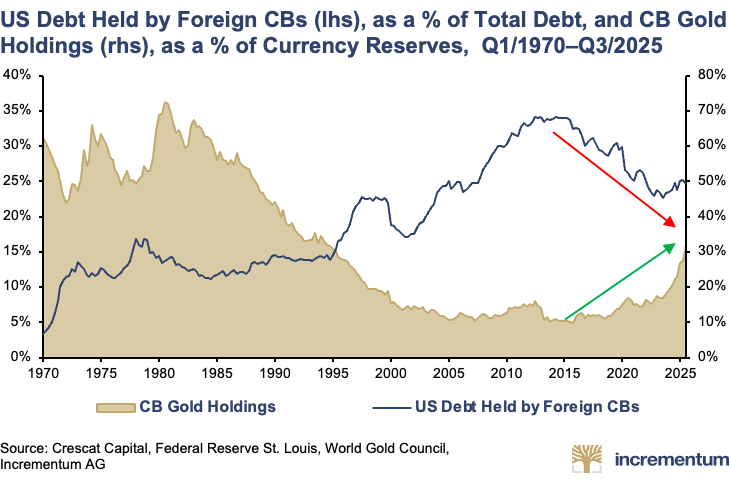

This gradual shift is evident in the composition of global currency reserves: While the share of US Treasury bonds held by foreign central banks has been declining for years, gold is once again gaining importance as a reserve asset. In 2007, the US dollar accounted for two-thirds of global currency reserves. That share now stands at less than 58%. When gold reserves are factored in, it drops to just around 45%. "We are observing a clear trend toward higher gold holdings in central banks' currency reserves. This development is driven both by ongoing gold purchases and by the significant appreciation of the gold price," says Mark Valek. "This is less a sudden vote of no confidence and more an expression of a growing need for geopolitically neutral reserves."

The Six Vectors of Gold Remonetization

The authors view gold's return to the center of the monetary order not as a singular event but as a process. While a new Bretton Woods moment seems unlikely given the geopolitical fragmentation, a series of structural shifts in reserve policy, accounting rules, institutional portfolios, and technological developments is far more plausible. The authors identify six key vectors of gold remonetization:

Reserve function & sovereignty: Gold as a sanctions-resistant, sovereign reserve asset and neutral store of value

Private and institutional demand: Gold is gaining strategic importance as a store of value

Accounting & recapitalization: Gold as a silent recapitalization option for central banks and governments

Anchoring in credit markets: Gold-backed bonds as a potential anchor of credibility for public finances

Accumulation: Western central banks as the potential next wave of buyers

Digitalization: Tokenization makes gold more mobile and tradable

"Gold is regaining importance wherever trust, security, or political neutrality are becoming scarcer," says Stöferle. The interplay of these developments is particularly relevant here. A rising gold price strengthens central bank balance sheets, increases the attractiveness of gold-linked financial instruments, and in turn accelerates strategic demand for gold.

"In addition to gold's growing importance as a reserve asset, its potential role as a settlement asset in international trade is also gaining relevance in the long term," adds Valek. "Particularly in the context of the BRICS countries and an increasingly multipolar world order, greater use of gold in cross-border payments seems far more likely today than it did just a few years ago."

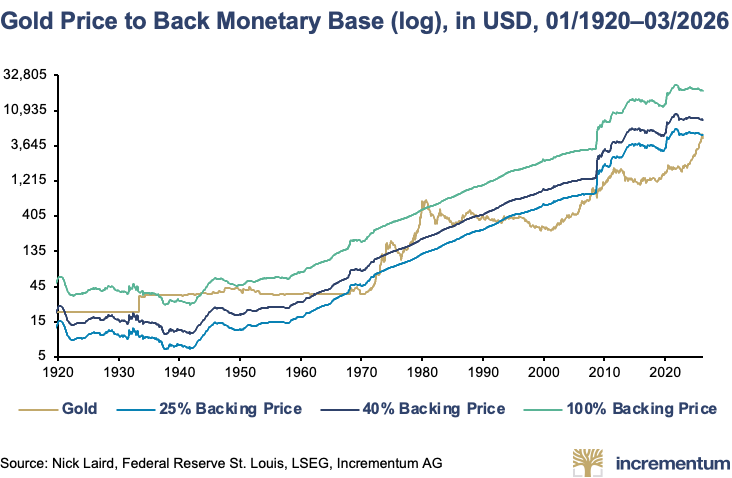

Should gold return to the center of the monetary system, the question of price consequences inevitably arises. An exact valuation is, by nature, impossible, but analytical approximations at least give us an idea of possible orders of magnitude. The best-known concept is the so-called shadow gold price, which indicates the theoretical gold price at which the monetary base would be fully backed by gold.

The reciprocal of the shadow gold price, based on current market prices, yields the gold coverage ratio of the monetary base. During the gold bull market of the 2000s, this ratio tripled from 10.8% to 29.7%. In the 1930s and 1940s, as well as in 1980, the gold coverage ratio was even above 100%. The record high of 131% from 1980 would correspond to a gold price of around USD 27,000. Currently, the gold coverage ratio of the US dollar equals just 22.4%. To put it bluntly: Less than a quarter of every US dollar is backed by gold - the remaining three-quarters are worthless.

The shadow gold price reveals two things: first, the enormous expansion of the money supply relative to the available amount of gold, and second, the long-term appreciation potential of gold should it - as described in the vectors outlined above - gradually regain monetary functions.

The Geopolitical Showdown and Gold's Margin Call

According to the authors, following the strong rally in the second half of 2025 and first quarter of 2026, a consolidation in the gold market was technically overdue. It was triggered by the escalation surrounding the Iran conflict. Instead of another price surge, there was a sharp correction and a global wave of deleveraging.

In March 2026, gold recorded its largest absolute monthly decline in its history, falling by USD 611. Calculated from its all-time high, the drawdown amounted to around 27%. For the authors, however, this is not a sign of structural weakness but rather a familiar pattern of acute liquidity crises.

"During periods of stress, gold is often sold not despite its strength, but precisely because of its high liquidity," explains Ronald-Peter Stöferle. "We observed the same pattern back in 2008 during the Lehman crisis as well as in the 2020 Covid-19 crash."

Rising yields, a stronger US dollar, and a wave of margin calls and forced liquidations had a particularly negative impact. At the same time, the closure of the Strait of Hormuz cut off important cash flows to the Gulf states, which had recently been accumulating gold at an increased rate.

From the authors' perspective, however, this is the real catalyst for gold: Historically, such periods of stress have usually been followed by expansionary monetary and fiscal policy measures. After 2008 and 2020, central banks responded with massive liquidity injections and a further expansion of their balance sheets. "The reaction of central banks remains a key driver for gold in the medium term," says Mark Valek. "Liquidity-driven pullbacks are not a contradiction to the long-term bull market but are often part of precisely the dynamics that structurally support gold."

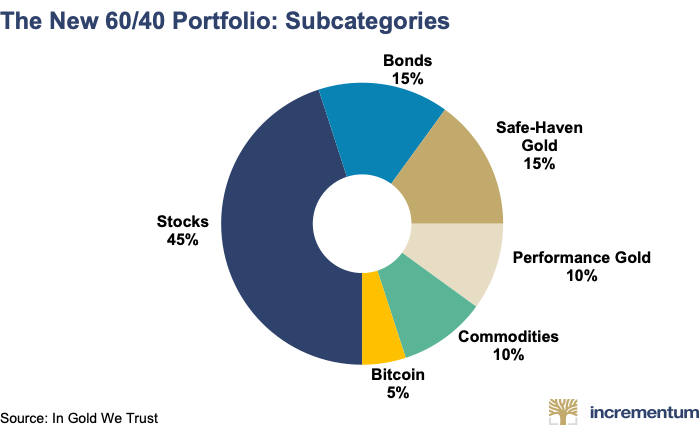

The new 60/40 portfolio is gaining importance

As early as in the In Gold We Trust report 2024, the authors presented their concept of a "new 60/40 portfolio": moving away from nominal claims toward noninflationable real assets. In addition to physical gold, silver, mining stocks, commodities, and Bitcoin play strategic roles, while the importance of traditional government bonds declines.

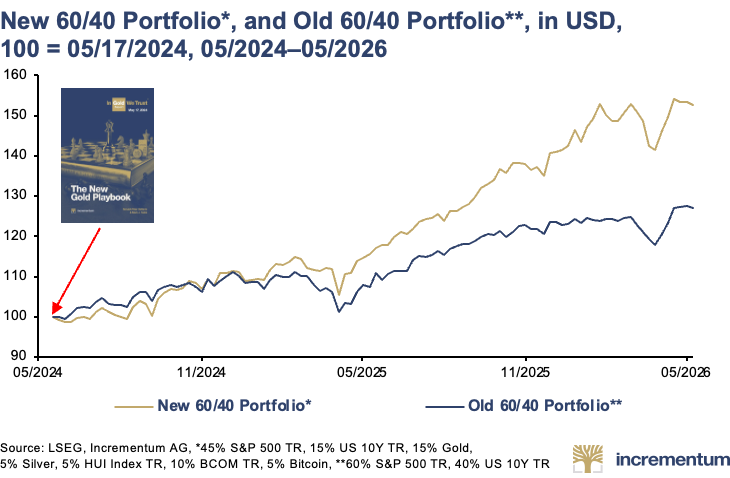

"The crucial question of this decade is no longer just what returns bonds yield, but how secure their real purchasing power actually still is," says Ronald-Peter Stöferle. Meanwhile, similar voices are also growing on Wall Street. Morgan Stanley, for example, recently proposed a "60/20/20" portfolio with a 20% weighting in gold. According to the authors, the rationale behind this is the increasing fragility of the traditional 60/40 model in an environment of structurally higher inflation and growing fiscal risks. In 2022, the traditional 60/40 portfolio recorded a real return of -17.1%. During the last major inflationary era, the 60/40 portfolio recorded seven years of negative real returns, five of which saw losses exceeding 10%. The historical pattern mirrors today's stress factors.

"A robust portfolio today needs a stronger foundation," explains Mark Valek. "Don't put all your eggs in the gold basket - but focus more on hard money assets." Since the introduction of the new 60/40 model portfolio, it has outperformed the classic 60/40 portfolio by a wide margin.

Against this backdrop, the question increasingly arises as to what impact even moderate reallocations of institutional portfolios toward noninflationary assets would have. The scale of the figures is striking: The global bond market currently amounts to around USD 140trn, while the investable financial gold market is only about USD 15trn. A reallocation of just 2% from global bonds would amount to nearly USD 3trn - roughly one-fifth of the entire investment gold market. Even small reallocations could therefore have a significant impact on the price of gold.

Performance Gold and Commodities: The Return of Real Assets

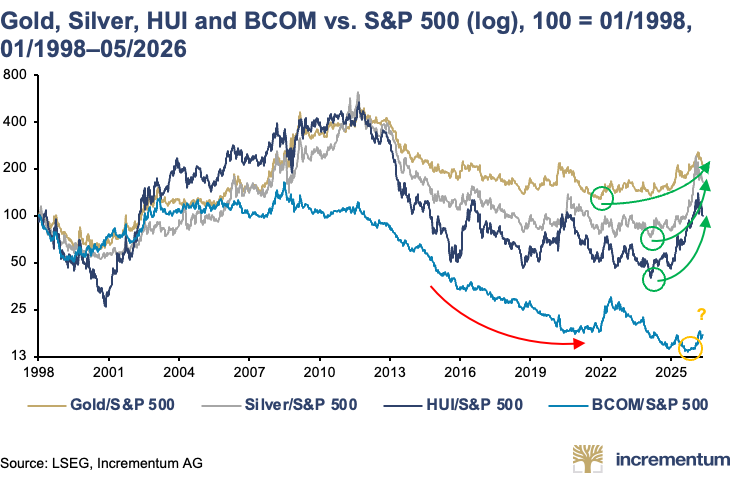

What the authors had already highlighted in the In Gold We Trust report 2025, The Big Long, has now partly come to pass: Gold has led the way, and silver, mining stocks, and commodities are now increasingly following suit. All major performance gold segments are now showing relative strength compared to the S&P 500 and point to a possible redistribution of global capital flows.

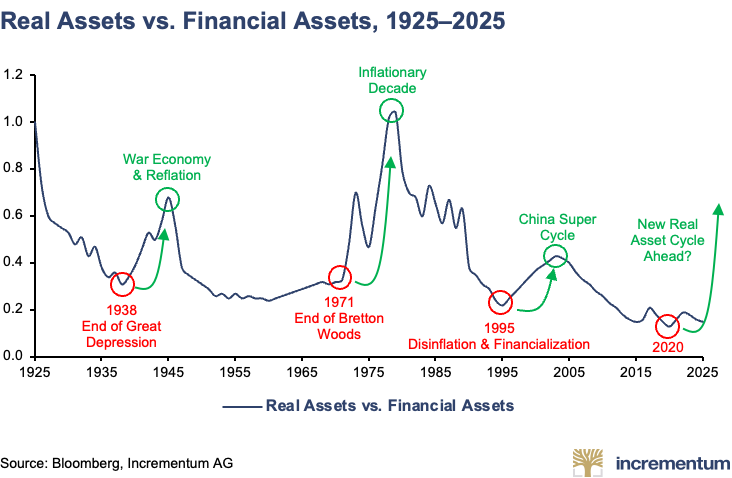

"Gold has paved the way; now silver, mining stocks, and commodities are increasingly catching up," explains Ronald Stöferle. A long-term historical analysis shows that phases of extreme dominance by financial assets have regularly been followed by extended periods of relative strength in real assets. From the authors' perspective, the trend that began in 2020 could mark the start of a new cycle for real assets - driven by inflation, geopolitical fragmentation, and the return of strategic commodity and gold allocations.

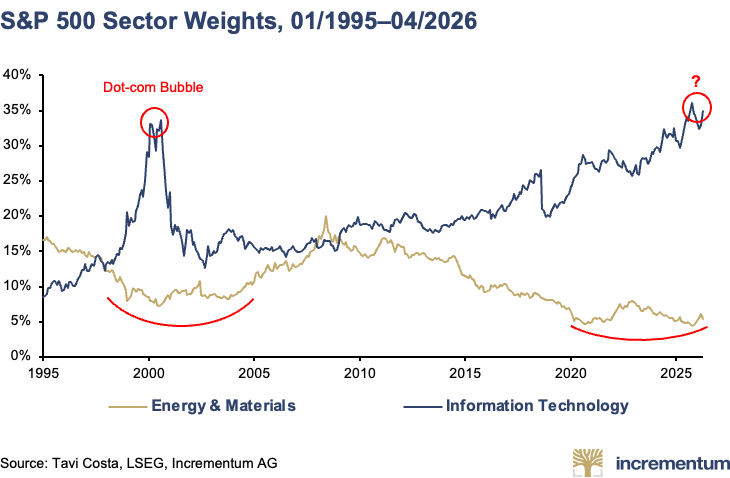

"The world is returning from financial to physical reality," says Mark Valek. "It is no longer ‘wanting' but ‘having' that increasingly determines growth." Particularly noteworthy, he notes, is the continued low weighting of traditional commodity sectors in the stock markets. Energy and materials companies currently account for less than 6% of the S&P 500. Even moderate shifts in capital allocation by institutional investors could therefore have a significant impact on price trends.

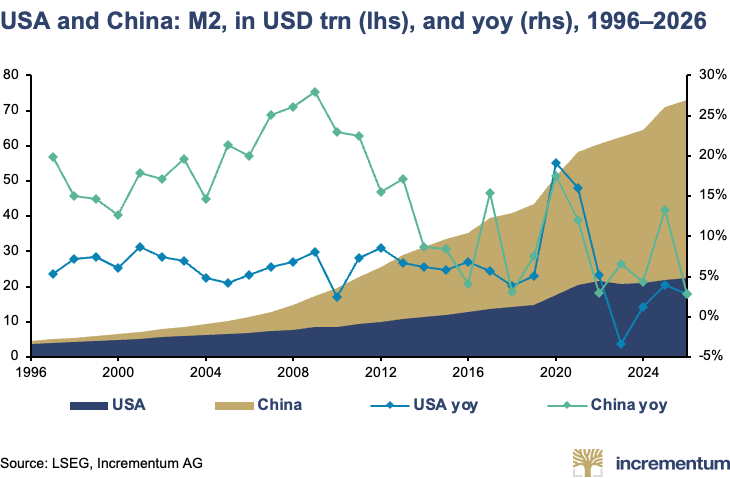

According to the authors, China also remains a key driver of the commodity cycle. High money supply expansion, along with a strategic focus on industrial sovereignty and infrastructure investments, continues to support the entire hard-asset sector.

"The commodity bull market is likely only at the beginning of a broader uptrend," explains Valek.

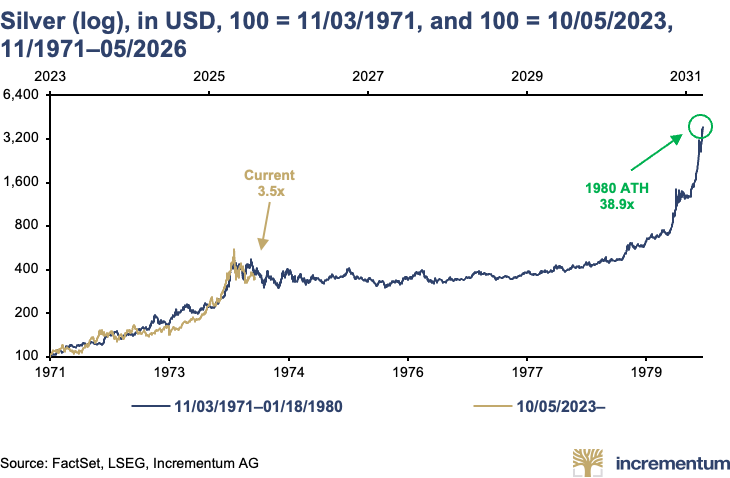

The authors continue to view silver particularly positively. In 2025, silver posted its strongest annual performance since 1979 at +146.8% and broke through the USD 100 mark for the first time in early 2026. The silver market is characterized by supply shortages; at the same time, the energy transition, military buildup, and demand for alternative stores of value are all competing for a supply that reacts only sluggishly, because around 74% of silver is mined as a byproduct of other metals. "The structural deficits in the silver market were ignored for years - until the market suddenly reacted," says Ronald-Peter Stöferle.

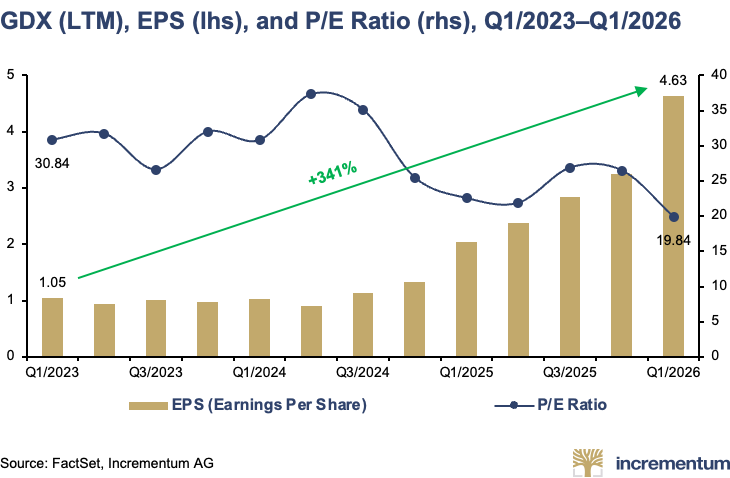

The authors see meaningful upside potential in gold mining stocks. AISC margins are nearly USD 3,000/oz, and balance sheets are solid. The free cash flow margin of the GDX Index rose from 4.2% to 24.5% between Q1/2023 and Q1/2026, with earnings per share quadrupling from USD 1.05 to USD 4.63, even though the P/E ratio fell from 30.8x to 19.8x.

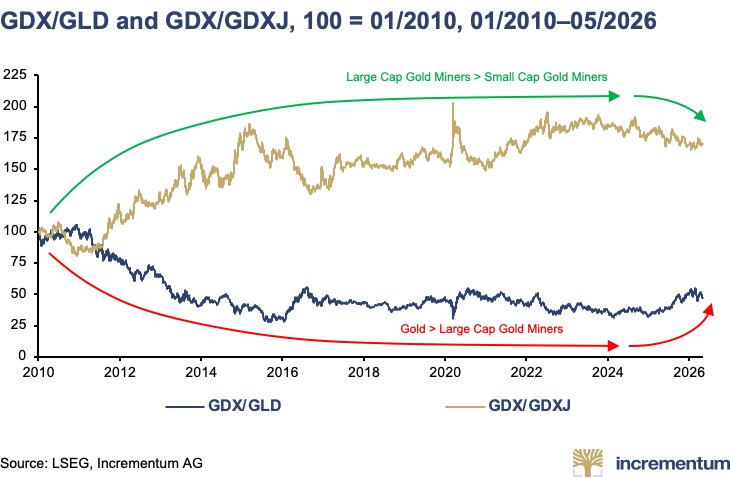

Small- and mid-cap mining stocks, in particular, could benefit disproportionately in the event of a broader rotation into the commodities and precious metals sectors.

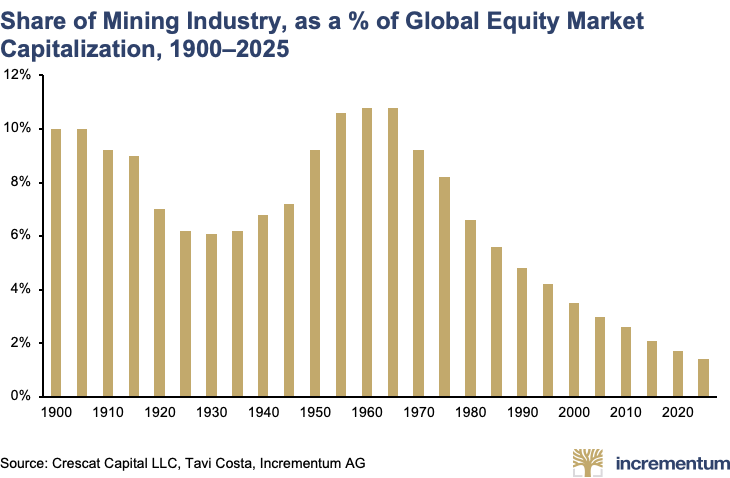

Nevertheless, the entire sector remains a minnow: The ten largest gold mining companies have a combined market capitalization of around USD 500 bn, accounting for only about 1% of global stock market capitalization.

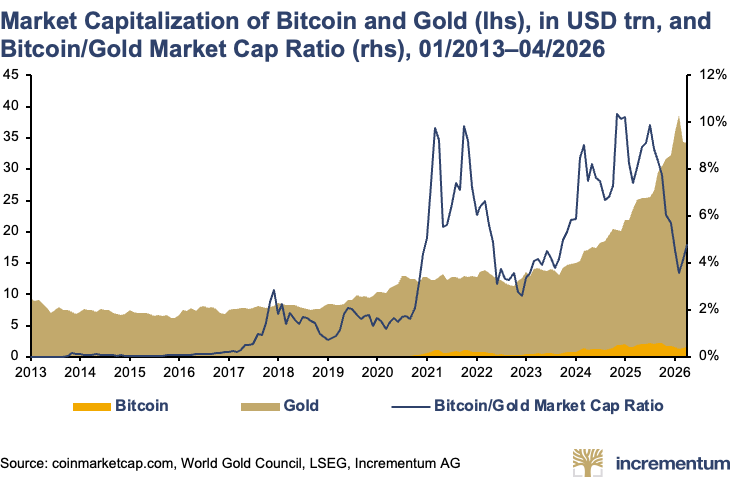

Gold and Bitcoin: Competition or Symbiosis?

In the authors' view, the growing monetary significance of gold could also act as a catalyst for Bitcoin in the long term. With the introduction of strategic Bitcoin reserves by the US, competition for monetarily scarce assets has reached a new dimension. Governments hold approximately 643,000 BTC, which corresponds to about 3.1% of the total supply. If one were to use the central banks' 17% share of above-ground gold reserves as a basis, this would imply government inflows of around USD 253bn. "What gold regains in monetary significance could also boost Bitcoin's value in the long term," explains Mark Valek. "Because a rising gold price simultaneously increases attention on digitally scarce and state-independent assets."

The authors confirm that they view gold and Bitcoin less as rivals and increasingly as complementary components of the same asset class. While gold primarily embodies stability and monetary history, Bitcoin stands for mobility, technological innovation, and convexity. "Gold represents monetary stability, Bitcoin monetary optionality," Valek continues.

Despite its strong growth in terms of market capitalization, Bitcoin still accounts for only a fraction of the gold market. Following the recent correction, Bitcoin currently appears relatively undervalued compared to gold, which, in the authors' view, further underscores the digital asset's long-term catch-up and convexity potential.

The authors view the growing institutional acceptance of combined gold-Bitcoin strategies - such as through new fund and ETF solutions - as an important structural trend.

"More and more investors are recognizing that gold and Bitcoin are often more resilient together than when considered in isolation," explains Valek. "We can also observe this in our own fund strategies, which combine precious metal investments with Bitcoin exposure and which we have been managing for over six years now. These are now attracting interest from a significantly broader range of investors."

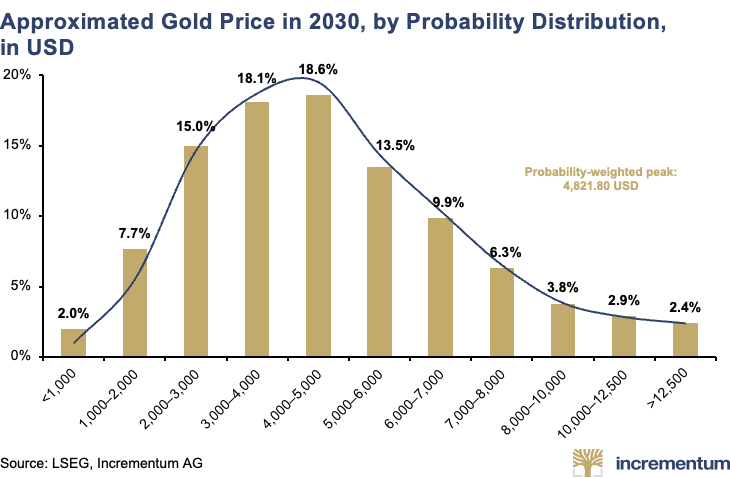

The Decade Price Target: Base-Case Scenario of USD 4,800 Reached, USD 8,900 in Focus

In the In Gold We Trust report 2020, "The Golden Decade," the authors presented their proprietary Incrementum gold price model, which simulates various scenarios regarding money supply growth and implied gold backing. The baseline scenario at that time - a gold price of USD 4,800 by the end of 2030 - was already reached in 2026. "The fact that our conservative decade-end target was reached so early underscores the momentum of current monetary and geopolitical developments," explains Ronald-Peter Stöferle.

Against the backdrop of persistent inflation and debasement risks, the authors are now increasingly focusing on the alternative inflationary scenario, with a gold price target of USD 8,900 by the end of the decade. As of April 30, gold was trading only slightly below the calculated interim target for the end of 2026.

The model deliberately accounts for this possibility through a heavily right-skewed probability distribution. Particularly in the event of pronounced remonetization trends and an accelerated erosion of confidence in fiat currencies, the authors see significantly greater upside potential than downside risk in the long term. Extreme upward movements are entirely conceivable during monetary transition phases. "Should the remonetization of gold continue to accelerate, we believe significantly higher price levels are possible in the long term," said Mark Valek.

In the short term, the outlook for gold is likely to remain challenging amid rising bond yields and elevated market volatility. In particular, rising long-end yields competing with increasing inflation rates could create temporary headwinds. "Liquidity-driven corrections are nothing unusual in advanced bull markets," explains Ronald-Peter Stöferle. "However, such pullbacks do not change our long-term constructive view on gold's structural investment case."

About the In Gold We Trust report

This annual gold study has been written by Ronald-Peter Stöferle for 20 years and together with Mark Valek since 2013. It provides a holistic assessment of the gold sector, including the most important influencing factors, such as the development of real interest rates, opportunity costs, debt, and monetary policy. The study is regarded as an international standard work for gold, silver, and mining stocks. In addition to German and English versions, the short version of the In Gold We Trust reportis also published in Spanish and Japanese. The Chinese version will be published for the seventh time this fall.

The publishing rights for the In Gold We Trust report were transferred to Sound Money Capital AG in November 2023. The In Gold We Trust report will continue to be co-branded with the Incrementum brand as usual.

The following internationally renowned companies have been won as Premium Partners for the In Gold We Trust report 2026: Agnico Eagle Mines, Argenta Silver, Asante Gold, Barrick, Caledonia Mining, Cerro de Pasco Resources, Elemental Royalty, Elementum, Endeavour Mining, Endeavour Silver, Equinox Gold, First Majestic Silver, First Mining Gold, Fortuna Mining, Harmony, Kinross Gold, Luca Mining, McEwen, Mineros, Münze Österreich, Newmont, North Peak Resources, Ögussa, Pan American Silver, Pinnacle Silver and Gold, Royal Gold, Solit, Sprott, Tudor Gold, U.S. Gold, Von Greyerz

The In Gold We Trust report 2026 will be published in the following issues:

Starting this year, a print version of the In Gold We Trust report can be purchased via Amazon:

Video of the press conference - English

Video of the press conference - German

All previous issues of the In Gold We Trust report can be found in our archive.

The authors

Ronald-Peter Stöferle is Managing Partner & Fund Manager of Incrementum AG.

Previously, he was part of the research team at Erste Group in Vienna for seven years. Starting in 2007, he began publishing his annual In Gold We Trust report, which has gained international renown over the years.

Together with Rahim Taghizadegan and Mark Valek, he published the bestseller Austrian School for Investors in 2014. In 2019, he co-authored The Zero Interest Trap. He is a member of the boards of Tudor Gold and Goldstorm Metals and has been an advisor to VON GREYERZ AG since 2020 and to Monetary Metals since 2024.

Mark Valek is Partner & Fund Manager at Incrementum AG.

Prior to that, he worked at Raiffeisen Capital Management for over ten years, most recently serving as a fund manager in the Multi-Asset Strategies department. In this position, he was responsible for inflation hedging strategies and alternative investments and managed portfolios with a volume of several hundred million euros.

Together with Rahim Taghizadegan and Ronald-Peter Stöferle, in 2014 he published the book Austrian School for Investors. He has been active as an entrepreneur on several occasions and was co-founder of philoro Edelmetalle GmbH. Since 2024 Mark has held the position of an advisor to Monetary Metals.

Incrementum AG

Incrementum AG is an independent investment and asset management company based in the Principality of Liechtenstein. The company was founded in 2013. Independence, reliability, and autonomy are the cornerstones of the company's philosophy. The company is wholly owned by the five partners.

Publisher

Sound Money Capital AG

Industriering 21

FL-9491 Ruggell

Principality of Liechtenstein

E-mail: [email protected]

Webpage: www.ingoldwetrust.report

Press information (photos, press release): www.ingoldwetrust.report/press

Disclaimer:

This publication is for information purposes only and does not constitute investment advice, investment analysis, or an invitation to buy or sell financial instruments. In particular, this document is not intended to replace individual investment advice or other professional guidance. The information contained in this publication is based on the state of knowledge at the time of preparation and may be changed at any time without further notice.

The publishing rights for the In Gold We Trust Report were transferred to Sound Money Capital AG in November 2023. Furthermore, the report continues to be co-branded with the Incrementum brand, as it has been in the past.

The authors have taken the greatest possible care in selecting the sources of information used and (like Sound Money Capital AG and Incrementum AG) accept no liability for the accuracy, completeness or timeliness of the information or sources of information provided or for any resulting liability or damages of any kind (including consequential or indirect damages, loss of profit or the occurrence of forecasts made).

All publications of Sound Money Capital AG and Incrementum AG are, in principle, marketing communications or other information and not investment recommendations within the meaning of the Market Abuse Regulation. Neither company publishes investment recommendations.

Sound Money Capital AG is wholly and exclusively responsible for the content of this In Gold We Trust Report.

Copyright: 2026 Sound Money Capital AG. All rights reserved.

SOURCE: In Gold in Trust