Friday, 22 May 2026 02:25 AM

Company Update

The glass container market is transforming into a sustainability-driven packaging solution, fueled by premium branding, recyclability, product protection, and circular economy initiatives.

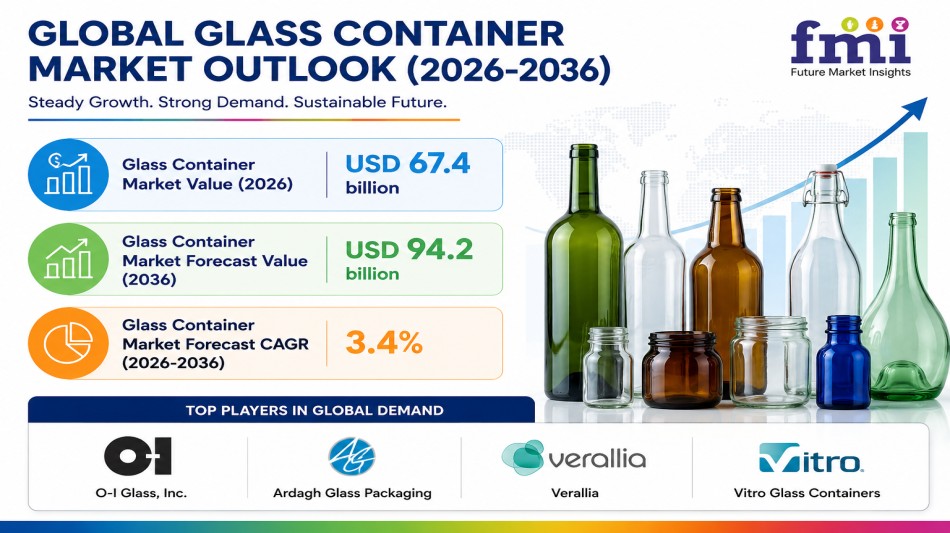

NEWARK, DE / ACCESS Newswire / May 22, 2026 / According to the latest market analysis by Future Market Insights, the glass container market is transitioning from a conventional packaging format into a strategic brand protection and sustainability-driven packaging solution. Valued at USD 65.2 billion in 2025 and projected to reach USD 67.4 billion in 2026, the market is expected to expand at a CAGR of 3.4% during the forecast period, ultimately reaching USD 94.2 billion by 2036.

This growth reflects a structural shift in packaging priorities across beverage, food, pharmaceutical, and beauty industries, where product protection, recyclability, and premium shelf appeal are becoming central purchasing criteria.

Quick Stats at a Glance

Market size (2025): USD 65.2 billion

Estimated value (2026): USD 67.4 billion

Forecast (2036): USD 94.2 billion

CAGR (2026-2036): 3.4%

Leading material: Soda lime glass (68.0% share)

Dominant neck type: Narrow neck containers (58.0% share)

Top product type: Bottles (52.0% share)

Leading application: Pharmaceuticals (48.0% share)

Key technology trend: Light weighting technology (42.0% share)

Fastest-growing markets: India (6.0%), China (5.3%)

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.futuremarketinsights.com/reports/sample/rep-gb-935

Market Size and Structural Shift

The glass container market is entering a long-term modernization cycle as packaging evolves beyond basic storage into a brand credibility and compliance-focused solution.

Historically, glass containers were selected mainly for durability and product storage. Today, purchasing decisions increasingly depend on recyclability credentials, premium presentation, chemical resistance, and compatibility with circular packaging systems.

Beverage brands continue to anchor demand, particularly in beer, spirits, and premium soft drinks, where glass preserves flavor integrity while enhancing shelf visibility. Meanwhile, pharmaceutical and beauty brands are elevating the value proposition of glass through high-quality vials, ampoules, perfume bottles, and cosmetic jars.

The market is also benefiting from investments in lightweight container technology and hybrid furnace systems that reduce transport costs and carbon emissions without compromising packaging quality.

Growth Drivers: Premiumization, Recycling, and Product Protection

Three major forces are accelerating global demand for glass containers.

1. Premium Beverage Packaging Expansion

Alcoholic beverage producers continue to rely heavily on glass packaging because it protects taste while reinforcing premium branding. Craft beer, wine, spirits, and specialty beverage brands increasingly prefer glass for high-end product positioning.

2. Sustainability and Recycling Regulations

Global packaging regulations are reshaping procurement strategies. The European Union's Packaging and Packaging Waste Regulation (PPWR) is pushing packaging suppliers to demonstrate recyclability and reuse compatibility ahead of stricter enforcement timelines.

Glass benefits from established recycling systems and high collection rates in many developed markets, making it attractive for brands seeking long-term compliance stability.

3. Rising Pharmaceutical and Beauty Packaging Demand

Pharma manufacturers require chemically stable packaging formats for syrups, injectable medicines, and sensitive liquid formulations. Beauty and cosmetics brands also favor glass for premium packaging aesthetics and improved product preservation.

These applications generate higher-value demand compared to standard food packaging categories.

Market Constraints: Energy Costs and Furnace Investments

Despite stable growth prospects, the industry faces operational challenges.

Glass manufacturing remains energy intensive. Furnace operations require high-temperature melting systems, creating significant exposure to energy price fluctuations and carbon reduction pressures.

Large-scale furnace upgrades also demand substantial capital investment, making modernization difficult for smaller regional producers.

In addition, maintaining consistent color quality, wall thickness, and defect-free output requires advanced process control and stable recycled cullet supply.

As a result, supplier competitiveness increasingly depends on operational efficiency rather than production scale alone.

Opportunity Landscape: Where Growth Is Emerging

Several strategic opportunities are shaping the next phase of market expansion:

Low-carbon furnace technologies: Hybrid and NextGen furnace systems are helping suppliers reduce emissions while maintaining output quality.

Lightweight glass packaging: Brands are reducing material usage and freight costs through ultra-light container designs.

Premium decoration capabilities: Cosmetic and spirits brands increasingly demand embossed, decorated, and customized glass packaging.

Circular packaging programs: Deposit-return systems and reusable bottle networks are supporting long-term container demand in mature markets.

Pharma-grade specialty packaging: High-value vials and ampoules continue to create premium-margin opportunities for suppliers with advanced quality systems.

Segment Insights: Where the Market Is Concentrated

By Product Type: Bottles are expected to account for 52.0% of market demand in 2026, supported by beverage filling lines and liquid pharmaceutical packaging requirements.

By Material: Soda lime glass is forecast to hold 68.0% share in 2026 due to its cost efficiency, forming performance, and suitability for food and beverage applications.

By Application: Pharmaceuticals are expected to represent 48.0% share in 2026 as drug manufacturers prioritize chemically stable and contamination-resistant packaging formats.

By Technology: Light weighting technology is projected to account for 42.0% of demand in 2026 as manufacturers seek lower transport costs and reduced raw material consumption.

By Neck Type: Narrow neck containers are anticipated to hold 58.0% share in 2026 because beverage filling systems require secure sealing and efficient high-speed line compatibility.

Speak to Analyst: Customize insights for your business strategy:

https://www.futuremarketinsights.com/customization-available/rep-gb-935

Regional Dynamics: Growth Varies Across Markets

Demand patterns differ significantly by region depending on recycling systems, beverage production, and pharmaceutical manufacturing capacity.

India (6.0% CAGR): India is expected to emerge as the fastest-growing market due to expanding pharmaceutical production, rising beverage consumption, and investments in local container manufacturing capacity.

China (5.3% CAGR): China continues to benefit from large-scale beverage and food packaging demand, supported by cosmetics and export-oriented manufacturing.

Canada (2.9% CAGR): Strong deposit-return systems and circular packaging programs are helping sustain long-term bottle demand across beverage categories.

United States (2.5% CAGR): Demand remains supported by craft beverages, premium spirits, and pharmaceutical packaging replacement cycles.

Germany (2.0% CAGR): Advanced recycling infrastructure and reusable beverage packaging systems continue to strengthen glass adoption despite energy-cost pressures.

Competitive Landscape: Sustainability and Reliability Define Leadership

The competitive environment is shifting toward operational reliability, low-emission production, and premium-quality output.

Leading companies including O-I Glass, Inc., Ardagh Glass Packaging, Verallia, Vitro Glass Containers, BA Glass, Vidrala, and PGP Glass Pvt. Ltd. are increasingly differentiating through:

Low-emission furnace technologies

Recycled cullet integration

Decorative and premium packaging capabilities

Pharma-grade quality control systems

Broad regional manufacturing networks

Faster mold turnaround and technical support

For buyers, reliable supply continuity and sustainability documentation are becoming as important as pricing.

Strategic Implications for Industry Stakeholders

For manufacturers, future competitiveness will depend on furnace efficiency, recycled material access, and premium packaging specialization.

For beverage and food brands, glass containers remain a strategic tool for premium positioning, recyclability claims, and flavor protection.

For pharmaceutical companies, demand for high-quality vials and ampoules will continue to support higher-margin packaging programs.

For investors, long-term opportunities are emerging around lightweight technology, low-carbon furnace systems, and circular packaging infrastructure.

For procurement leaders, supplier evaluation is increasingly focused on compliance readiness, recycling proof, and operational stability.

Future Outlook: From Packaging Material to Circular Packaging Platform

Over the next decade, glass containers are expected to evolve from standard packaging components into integrated circular-economy packaging assets.

Key trends shaping the future include:

Expansion of hybrid and low-carbon furnace systems

Greater use of recycled cullet in commercial production

Wider adoption of lightweight premium glass formats

Growth in reusable and refillable bottle systems

Increased use of smart packaging and digital traceability technologies

Stronger integration between sustainability reporting and packaging procurement

As sustainability regulations intensify and premium packaging demand rises, glass containers are expected to remain a critical packaging format across beverage, pharmaceutical, and beauty industries.

Unlock 360° insights for strategic decision making and investment planning-

https://www.futuremarketinsights.com/checkout/935

Executive Takeaways

Glass containers are evolving from basic storage packaging into premium brand protection solutions.

Sustainability regulations and recycling mandates are strengthening long-term demand.

Beverage, pharmaceutical, and beauty industries remain the market's core growth engines.

Lightweight technology and low-carbon furnace investments are reshaping supplier competitiveness.

Operational reliability, recycled material access, and compliance proof are becoming decisive procurement factors.

The next phase of market growth will be driven by circular packaging systems and low-emission production technologies.

Related Reports:

Glass Bottle and Container Market: https://www.futuremarketinsights.com/reports/glass-bottle-and-container-market

Glass Frosting for Packaging Market: https://www.futuremarketinsights.com/reports/glass-frosting-for-packaging-market

Glass Bottles Market: https://www.futuremarketinsights.com/reports/glass-bottles-market

Glass Liquor Bottle Market: https://www.futuremarketinsights.com/reports/glass-liquor-bottles-market

Glassine Paper Market: https://www.futuremarketinsights.com/reports/glassine-paper-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - [email protected]

For Media - [email protected]

For Web - https://www.futuremarketinsights.com/

For Web - https://www.factmr.com/

SOURCE: Future Market Insights, Inc.