Thursday, 21 May 2026 09:35 AM

Company Update

Additively Manufactured Drivetrain Brackets and Housings Market Accelerates as EV Lightweighting, Metal Additive Manufacturing, and Production-Grade Component Qualification Reshape Next-Generation Vehicle Engineering

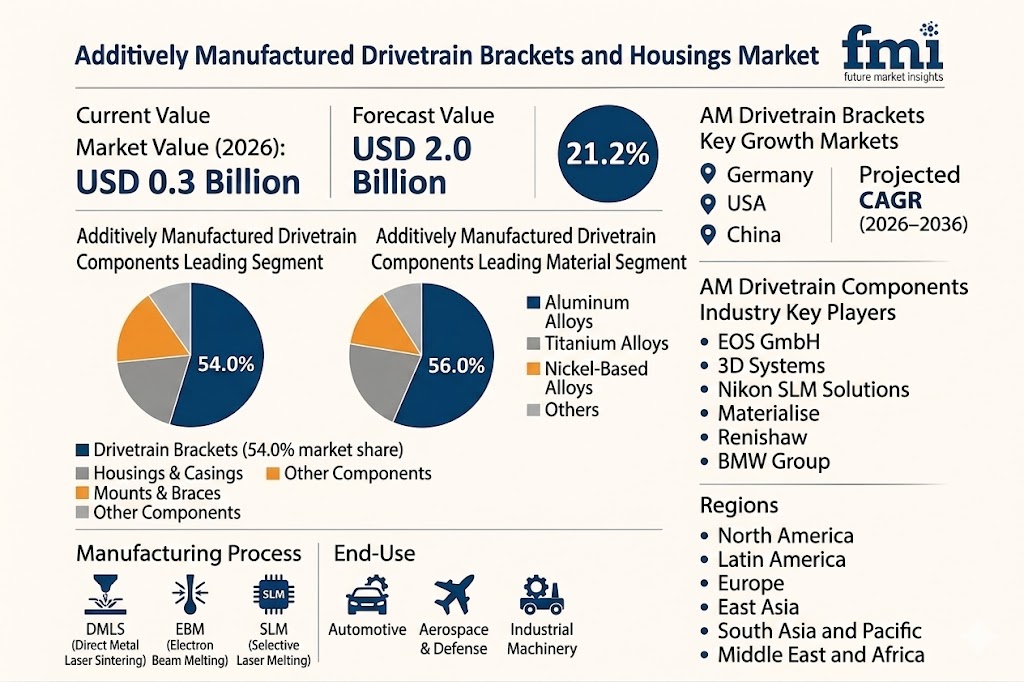

NEWARK, DE / ACCESS Newswire / May 21, 2026 / According to the latest analysis by Future Market Insights, the global automotive manufacturing sector is entering a decisive transformation phase where digital production, lightweight engineering, and electrified mobility are reshaping component development strategies. The Additively Manufactured Drivetrain Brackets and Housings Market, valued at USD 0.3 billion in 2026, is projected to reach USD 2.0 billion by 2036, expanding at a robust CAGR of 21.2% during the forecast period.

The shift reflects more than enthusiasm around 3D printing-it signals a structural move toward production-ready additive manufacturing (AM) for critical automotive applications.

As electric vehicle architectures evolve and packaging constraints intensify, manufacturers are increasingly adopting additively manufactured drivetrain components to reduce mass, improve thermal management, accelerate development cycles, and eliminate unnecessary assembly complexity.

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.futuremarketinsights.com/reports/sample/rep-gb-33136

Market Metrics Snapshot (2026-2036)

Market Value (2026): USD 0.3 Billion

Forecast Value (2036): USD 2.0 Billion

Projected CAGR (2026-2036): 21.2%

Leading Component Segment: Drivetrain Brackets (54.0% market share)

Leading Material Segment: Aluminum Alloys (56.0% market share)

Leading Manufacturing Process: Powder Bed Fusion (45.0% market share)

Dominant Sales Channel: OEM Programs (82.0% market share)

Primary Growth Driver: EV Lightweighting & Design Consolidation

Moving Beyond Prototypes: Additive Manufacturing Enters Functional Vehicle Production

For years, additive manufacturing remained largely associated with prototyping and low-volume concept validation. In 2026, that narrative is changing rapidly.

Automotive OEMs and Tier 1 suppliers are increasingly applying metal additive manufacturing technologies to produce load-bearing drivetrain brackets, motor housings, e-axle carriers, and compact mounting systems that support evolving EV powertrain architectures.

Industry experts indicate that drivetrain applications represent one of the most commercially viable entry points for automotive metal AM due to their combination of geometric complexity and performance sensitivity.

"Automotive manufacturers are now evaluating additive manufacturing through measurable engineering outcomes rather than experimental capability. Weight reduction, assembly consolidation, and qualification repeatability are becoming the defining decision factors," notes an FMI industry analyst.

Engineering Efficiency Becomes the Primary Market Catalyst

Demand growth is closely tied to changing vehicle design priorities.

Electric drive modules place unprecedented pressure on space utilization, heat dissipation, and structural optimization. Traditional casting and machining approaches often create design limitations, while additive manufacturing enables engineers to develop topology-optimized geometries that conventional manufacturing cannot easily achieve.

Modern printed drivetrain components increasingly combine:

Structural ribs and mounting points into single consolidated parts

Optimized airflow and thermal pathways

Reduced material waste through near-net production

Faster design iteration through digital workflows

A major advantage of additive manufacturing lies in minimizing tooling dependency, allowing manufacturers to accelerate development cycles while preserving engineering flexibility.

Drivetrain Brackets Lead Commercial Qualification

Drivetrain Brackets Lead Adoption

Drivetrain brackets are projected to hold 54.0% market share in 2026.

Faster commercialization due to simpler qualification and lower sealing requirements than full housings.

Growing Demand for Advanced Housings

Motor housings and e-axle carriers are gaining traction.

Demand is driven by integrated thermal management and compact drivetrain packaging.

Aluminum Dominates Material Selection

Aluminum alloys are expected to capture 56.0% market share in 2026.

Preferred for lightweight performance, corrosion resistance, and EV compatibility.

Powder Bed Fusion Leads Manufacturing

Powder bed fusion (PBF) is forecast to account for 45.0% share.

Chosen for high precision and repeatable metal part production.

OEM Programs Drive Market Growth

OEM-led projects are projected to represent 82.0% of total demand.

Growth supported by strict engineering validation and controlled qualification processes.

Access the Complete Report in PDF Format: https://www.futuremarketinsights.com/reports/brochure/rep-gb-33136

Regional Momentum: China and India Set the Pace

Regional adoption patterns reveal significant differences in additive manufacturing maturity.

China is expected to emerge as the fastest-growing market, registering 23.5% CAGR through 2036, supported by expanding EV production capacity and growing domestic investment in industrial metal printing ecosystems.

Chinese manufacturers are increasingly integrating AM into vehicle development programs to reduce lead times and improve drivetrain packaging efficiency.

India, projected to expand at 22.8% CAGR, is becoming an increasingly important growth center due to government-backed EV manufacturing initiatives and rising localization of advanced automotive components.

Meanwhile:

United States: 20.4% CAGR supported by mature automotive engineering clusters

South Korea: 19.6% CAGR driven by compact EV drivetrain innovation

Germany: 19.2% CAGR supported by premium engineering and captive AM facilities

Mexico: 18.5% CAGR benefiting from North American nearshoring trends

Japan: 17.8% CAGR supported by selective, quality-driven adoption

Qualification and Economics Remain Critical Challenges

Despite strong growth momentum, commercialization barriers remain significant.

Qualification requirements for drivetrain applications continue to create long development cycles. Fatigue testing, thermal validation, dimensional control, and post-processing consistency remain essential before production approval.

Additionally, traditional cast and machined parts continue to set aggressive cost benchmarks.

Manufacturers must demonstrate clear value through:

Lower vehicle mass

Part consolidation benefits

Faster engineering iterations

Reduced assembly complexity

Improved supply chain responsiveness

Industry participants increasingly view repeatable material performance and documented process control as competitive differentiators.

Competitive Landscape: Industrial Ecosystems Take Shape

Competition is evolving beyond machine suppliers alone.

Market leadership increasingly depends on integrating software workflows, metal processing expertise, qualification systems, and production scalability.

Key industry participants include:

Metal AM Platform Providers

EOS GmbH

3D Systems

Nikon SLM Solutions

Workflow & Manufacturing Specialists

Materialise

Renishaw

GKN Additive

Automotive & Digital Production Leaders

BMW Group Additive Manufacturing Campus

Divergent Technologies

Precision Resource

Recent strategic developments indicate accelerating industrial readiness, including investments in serial metal production platforms, digital manufacturing expansion, and partnerships focused on high-criticality automotive components.

Buy Report: Unlock 360° insights for strategic decision making and investment planning:

https://www.futuremarketinsights.com/checkout/33136

Outlook: From Performance Programs to Mainstream Vehicle Platforms

By 2036, additively manufactured drivetrain brackets and housings are expected to transition from specialized engineering initiatives into broader production ecosystems.

As EV architectures become increasingly compact and automakers pursue measurable efficiency gains, additive manufacturing is positioned to become a practical production tool rather than an experimental technology.

The next phase of growth will likely belong to suppliers capable of delivering repeatable metal properties, validated manufacturing workflows, and scalable qualification processes-turning digital part files into production-ready vehicle components at industrial speed.

Related Reports:

Weld Angle Brackets Market- https://www.futuremarketinsights.com/reports/weld-angle-brackets-market

Noise Control System Market- https://www.futuremarketinsights.com/reports/noise-control-system-market

Vibration Control Systems Market- https://www.futuremarketinsights.com/reports/vibration-control-systems-market

Machine Control System Market- https://www.futuremarketinsights.com/reports/machine-control-system-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - [email protected]

For Media - [email protected]

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.